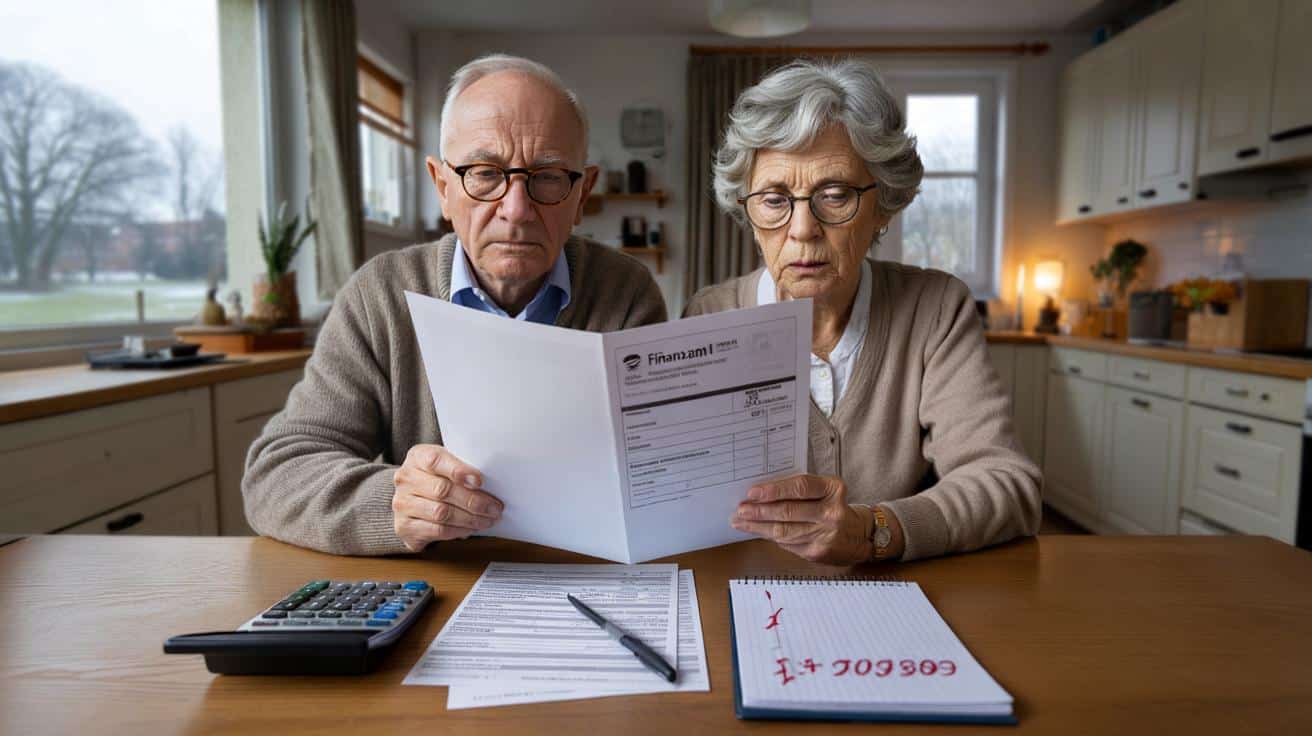

The letter doesn’t look dangerous at first. Thin white envelope, Finanzamt logo in the corner, a few dry lines about “Anpassung der Steuervergünstigung” and a date: 29. Februar. Yet at the kitchen table in countless German flats, retired people are sitting with this sheet of paper in their hands and a knot in their stomach. Annual income above 24,000 euros? Then the calm picture of a “safe” retirement starts to wobble a bit.

Suddenly there are questions: Did I claim too much relief? Do I now owe back taxes? Is my pension secretly “too high”?

The deadline is ticking, the language is technical, and the fear of making a mistake is very human.

Something here feels like a trap you never knew existed.

Was hinter der neuen Pflicht für Rentner wirklich steckt

Across Germany, tax offices are quietly reminding retired people with more than 24,000 euros in annual income that they must correct a tax relief by the end of February. Not a headline-grabbing scandal, more a bureaucratic tremor that only those affected feel. The rule targets people whose pensions, company pensions or other retirement income push them above this threshold.

On paper, it’s about “klarstellende Angaben” and a corrected tax relief. In real life, it’s about fear of surprise bills from the Finanzamt and the feeling of being left alone with dense legal German.

Take the story of Helga, 71, from near Cologne. She worked 42 years in administration, raised two kids alone, and now gets a statutory pension plus a small company pension. Her total: just over 25,000 euros a year. For her, that’s not luxury, it’s the line between “okay” and “tight at the end of the month”.

In January she received a notice: the previous tax relief had been granted too generously and must be corrected. Suddenly she reads about “Rentenfreibetrag”, “Versorgungsbezüge”, “Besteuerungsanteil”. She calls her daughter, then the hotline. Each answer raises a new question. The real shock isn’t the possible back payment. It’s the feeling that one wrong cross on a form could cost her hundreds of euros.

Behind this wave of letters sits a mix of digital data, changing pension taxation and the old idea that “pensions are tax-free” slowly dying. With more data flowing directly from pension insurance funds to the tax offices, discrepancies in tax reliefs are spotted faster. If your total annual pension income climbs above 24,000 euros, the Finanzamt looks more closely at whether previous tax advantages still fit the law.

This doesn’t mean every affected pensioner has cheated or made a mistake. Often, pensions have climbed slightly due to annual adjustments, or a small side income tipped the scale. *The tax system reacts slowly, but when it does, it rarely knocks gently.*

So gehen Rentner jetzt konkret mit der Februar-Frist um

The first step is painfully simple: open the letter and read it once, slowly, from top to bottom. Don’t jump straight to the euro amount. Look for three things: your recorded annual income, the description of the tax relief that needs correcting, and the mentioned deadline at the end of February. Lay this letter next to your latest pension notice and your last tax assessment.

Then grab a notepad. Write down: Which pensions do I receive? Statutory, company, private annuity, widow’s pension? Which amounts were reported in the last tax return? This little overview is your anchor. Without it, the forms turn into a fog.

➡️ Wie Sie mit einem Reisebudget-Tool Ihre Ausgaben kontrollieren und mehr von der Welt sehen

➡️ Wie eine einfache Zitrone drei verschiedene Putzmittel ersetzt

➡️ Die cleversten Möglichkeiten, um Platz in kleinen Wohnungen zu gewinnen

➡️ Einfacher Knopf im Auto kann die Frontscheibe enteisen, ohne dass Sie Eis abkratzen müssen

➡️ Warum das Vergessen von Namen bei neuen Bekanntschaften oft nichts mit dem Gedächtnis zu tun hat

Many retirees stumble at the same points. They underestimate so-called “Versorgungsbezüge” from former public-service jobs. They forget small extra incomes like a mini-job in the local shop or rental income from a tiny inherited flat. Or they still believe that anything called “pension” stays below the tax radar. We’ve all been there, that moment when you realize the rules quietly changed while you were busy just living your life.

This is where small mistakes snowball. A forgotten income here, a misunderstood line there, and the Finanzamt recalculates your relief less generously. That doesn’t mean you’re guilty, it just means the system doesn’t care about confusion.

The safest move for anyone close to or above 24,000 euros a year is to get a second pair of eyes on the numbers. That can be a Lohnsteuerhilfeverein, a tax advisor, or the tax counseling service of the pensioners’ association.

“People come to us with red cheeks and shaking hands,” says a volunteer at a local tax help association. “They are ashamed because they think they did something wrong. In most cases, they simply didn’t understand how quickly their taxable share of the pension rises.”

- Gather all documents: pension notices, last tax assessment, the new letter from the Finanzamt.

- Check if your total gross pension exceeds 24,000 euros a year and note all side incomes.

- Clarify whether the demanded correction only affects one relief or several past years.

- Ask for written clarification from the Finanzamt if a passage is unclear.

- Consider short, professional advice if the sum at stake is higher than one or two monthly pensions.

Was diese neue Steuerrealität für das Leben im Ruhestand bedeutet

This February deadline is more than a bureaucratic chore. It’s a sign that retirement in Germany is drifting further away from the old dream of “no more paperwork, just peace”. Tax rules, digital reporting and rising pensions intertwine, and those who cross the 24,000-euro line suddenly feel like accidental high earners. Let’s be honest: nobody really reads all those tax leaflets from cover to cover every single year.

Still, these letters force an uncomfortable but necessary question: What does “secure” income really mean if a part of it can evaporate through corrected tax reliefs? Some will share their stories with neighbors, others will quietly stack the notices in a drawer. And a few might start a new habit: putting a small slice of each monthly pension aside, not for holidays on the Baltic Sea, but for the next tax surprise.

The more these stories circulate, the less lonely they feel.

| Key point | Detail | Value for the reader |

|---|---|---|

| Frist bis Ende Februar | Rentner mit mehr als 24.000 € Jahresbezügen müssen eine korrigierte Steuervergünstigung erklären | Verhindert Verspätungszuschläge und unerwartete Nachzahlungen |

| Einkünfte genau prüfen | Gesetzliche Rente, Betriebsrente, Versorgungsbezüge und Nebenverdienste zusammentragen | Schafft Klarheit, ob man wirklich über der Schwelle liegt |

| Hilfe in Anspruch nehmen | Lohnsteuerhilfeverein, Steuerberater oder Beratungsstellen der Rentnerverbände nutzen | Reduziert Fehler, spart Zeit und oft auch Geld |

FAQ:

- Question 1Who exactly has to explain a corrected tax relief by the end of February?

- Question 2Does the 24,000-euro limit refer to gross or net pension income?

- Question 3What happens if I ignore the letter from the Finanzamt?

- Question 4Can I ask the Finanzamt for more time if I don’t get the documents together in time?

- Question 5Where can I get affordable help as a pensioner with a moderate income?