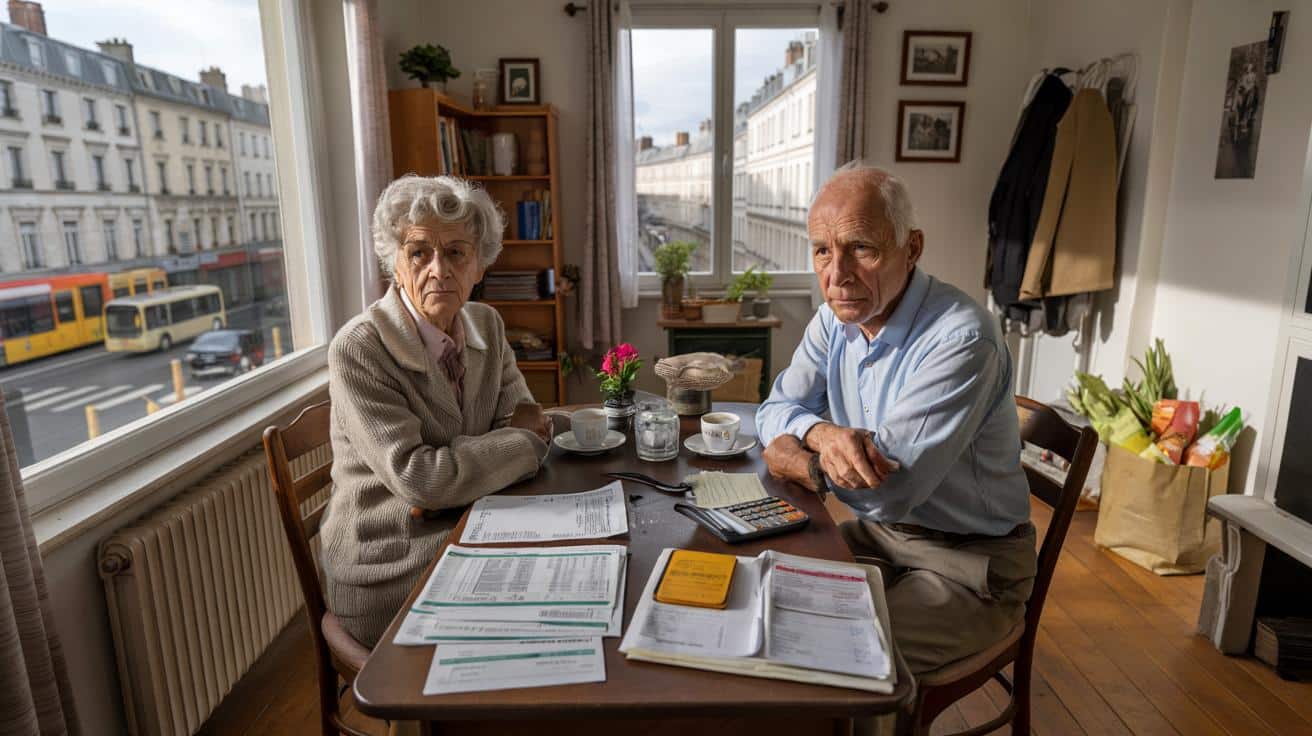

Behind the political slogans and pension reforms lies a more concrete issue: how much money does an older person actually need each month to eat properly, heat their home and still have a social life, without living on constant edge?

Living with dignity, not just getting by

French researchers and senior organisations insist on one point: “living with dignity” is not the same as scraping by with a roof and electricity.

For them, a dignified retirement includes basic comfort and a minimum of normal life: decent food, healthcare without postponing appointments, a warm home, public transport or a car, and the possibility of seeing friends or family and enjoying small leisure activities.

A “vital” retirement budget means paying for the essentials while keeping autonomy and a social life, not just avoiding destitution.

This nuance matters. With inflation pushing up food prices and energy costs, and with building maintenance charges increasing in many apartment blocks, retirees are often forced into trade-offs: turn down the heating, skip a dental appointment, or stop going out.

According to the French social ministries, nearly one in three retirees say they struggle to cover day-to-day expenses. The question of a minimum income for a “decent” retirement has become a social benchmark, even if it cannot capture every individual situation.

The key figure: 1,634 euros per month for a single homeowner

A study from the Institute for Economic and Social Research (IRES) tried to pin down a threshold. For a single retiree who owns their home outright in France, the estimate comes to €1,634 per month to “live decently”. That amount assumes no rent, but does include all the other costs of daily life.

This is what that budget is broadly designed to cover:

- Housing charges (taxes, building fees, energy)

- Food and basic household goods

- Health costs and top-up insurance

- Transport (public transport or car expenses)

- Leisure, outings and social activities

- Unexpected expenses and some savings

Set against this benchmark, the typical French pension looks tight. Official data (DREES) puts the average gross pension at about €1,626 a month, roughly €1,500 net. For a homeowner, that means the “average” pension barely reaches the IRES threshold.

➡️ Eine einfache Geste, damit Ihre Hortensien ihre Farbe auf natürliche Weise ändern

➡️ Wie du laut Psychologie in den ersten 5 Minuten eine schädliche Person erkennst

➡️ Why You Really Shouldn’t Air Out Your Home Between 8am and 10am in Winter

➡️ Acht Wege, ML-Modelle mit Sympy für transparente Mathe-Validierungen zu debuggen

For many retirees, the line between “just enough” and “not quite enough” is only a few tens of euros per month.

When rent enters the equation, the gap widens

The 1,634-euro figure assumes a retired person owns their home. That is a crucial detail. A tenant paying several hundred euros in rent faces a much higher threshold to enjoy the same standard of living.

Researchers generally estimate that tenants need several hundred euros more each month to maintain autonomy without heavy sacrifices. In big cities such as Paris, Lyon or Bordeaux, where rents are high and service charges are rising, the reality can be even harsher.

What a “comfortable” retirement looks like in numbers

Other studies give a sense of what many people would call not just “decent”, but genuinely comfortable. Various pieces of research place this level for a single retired person between €1,800 and €2,200 net per month.

That sort of budget typically allows:

| Spending area | What it usually covers |

|---|---|

| Housing | Charges, maintenance, local taxes, energy bills |

| Food | Balanced diet, some fresh produce, occasional meals out |

| Health | Top-up insurance, dental and optical care, regular check-ups |

| Transport | Public transport pass or running an older car |

| Leisure and social life | Clubs, cultural outings, short trips, hobbies |

| Safety margin | Repairs, replacement of appliances, small savings |

A separate barometer by Retraite.com and Silver Alliance looks specifically at the cost of “ageing well” at home. It estimates at around €1,291 per month the average cost of services helping older people stay in their own home, in addition to usual living expenses.

These services include help with housekeeping, small technical aids, home delivery, home adaptations and sometimes personal care. For many households, they come on top of already tight budgets.

Couples: shared costs, but double pressures

For couples, the picture is mixed. Housing and some bills are shared, which lowers the cost per person. Yet food, health and transport expenses often double, and care services for two people can quickly become expensive.

In rented accommodation or in expensive urban areas, even two pensions combined may struggle to cover both fixed charges and a real social life, especially if one partner has had a patchy career or long periods of part-time work.

When the pension falls short: options on the table

A significant portion of French retirees receive pensions under the 1,634-euro mark, especially women and those who worked on temporary or part-time contracts. For them, several mechanisms can help top up income.

State support and local aid

The main safety net is the Allocation de solidarité aux personnes âgées (ASPA). This allowance is designed to bring very low incomes up to a legal minimum for older people. It is means-tested and can be combined with a small pension.

On top of that, some retirees qualify for:

- Housing assistance such as APL (Aide personnalisée au logement)

- Support from local social action centres (CCAS) in towns and cities

- Department-level schemes for home help or transport

The French system offers several layers of aid, but they are scattered, complex and often underused by those who need them most.

Complementary income and late planning

Others choose to supplement their pension with small jobs: childcare, homework help, gardening or light DIY. Some rent out a spare room or part of their home, sometimes through intergenerational housing schemes where a student pays a modest sum in exchange for a room.

For people still working and getting close to retirement age, experts insist on anticipation. Products such as the French Plan Épargne Retraite (retirement savings plan) or life insurance policies allow workers to build an extra income stream for later years.

The goal is not luxury, but to reach that “vital” budget that makes it possible to choose where and how to live, rather than having every euro dictated by bills.

Why inflation hits retirees differently

Rising prices do not affect all age groups equally. Retirees, especially those on modest pensions, often dedicate a larger share of their income to essentials that are currently rising faster than average: food, energy and housing charges.

Health expenses also weigh more heavily with age. Even with the French public health system, co-payments, dental work or glasses can quickly eat into a monthly budget. When pensions are only partially indexed to inflation, purchasing power gradually erodes.

This slow erosion means that a pension that seemed just about adequate at 65 can feel clearly insufficient at 75 or 80, simply because everyday costs have crept upwards.

Concrete scenarios: what does “dignity” mean in practice?

Imagine a 72-year-old widow in a medium-sized French town, owning her flat and receiving €1,500 net per month. Her fixed charges – building fees, local taxes, energy – swallow almost half of it in winter. After groceries and health insurance, she still has a small margin for outings and gifts to grandchildren, but any major dental work or boiler breakdown forces her to cancel other spending for months.

Contrast that with a retired couple renting a flat in a large city, each with €1,100 net pension. Together they receive €2,200. Rent and charges approach €900, transport passes cost €150 for two, healthcare, insurance and food quickly take them down to a narrow leftover. They live decently day to day, but unexpected expenses almost always mean dipping into savings, when those exist.

Key notions worth knowing

Several terms often used in these debates can be confusing:

- Net pension: the amount actually received each month after social contributions.

- Standard of living: not just income, but what it allows in terms of housing, health, leisure and social participation.

- Dignified minimum: a benchmark defined by researchers based on real baskets of goods and services, not just a political slogan.

For households, using these notions can help structure their own calculations: list current and future expenses, factor in inflation, and compare them to likely pensions and savings. Even rough simulations can highlight gaps early enough to adjust work duration, savings habits or housing plans.

Behind the big national arguments about pension reforms, these concrete numbers – €1,634 for a single homeowner, €1,800–€2,200 for real comfort, plus extra for tenants and care services – show what is truly at stake: the ability for older people in France to age without fear of permanent deprivation.